Market Insights: A tale of two cities by Jeff Taylor

Two elections in one weekend are more than enough for any fund manager to cope with, the results coming out of Vienna and Rome being very different.

Let's get the Austrian Presidential election out of the way first. The independent candidate, Alexander van der Bellen, a former leader of the Green Party, beat his extreme right wing rival by a respectable margin. To be honest, we'd been struggling to understand why the media and some market commentators had been making quite so much of this election as a potential market moving event given the largely ceremonial status of Austria's president. However, as another reminder that political extremism is not guaranteed to win every time Europeans go to the polls, we'll take it.

Italy's Constitutional Referendum is of much greater significance for financial markets and there is no question that Renzi's defeat last night was by a wider margin than the polls had suggested. Renzi, as he said well in advance, will resign today.

However, that it's a No, cannot in itself be a surprise to anyone as opinion polls had been pointing firmly that way for a good few months. Partly for this reason, the Italian equity market has already been a major laggard this year. The main Italian equity index, the FTSE MIB, has underperformed the MSCI Europe ex UK index by 13.7% this year (in EUR, price return, as of Friday 2 December close). It's not just a reflection of the weakness of Italian banks either - look for example at ENI, the Italian oil major, which has already underperformed its sector (STOXX Europe 600 Oil & Gas) by 13% (in EUR, price return) so far this year, to our minds largely because it has an Italian passport.

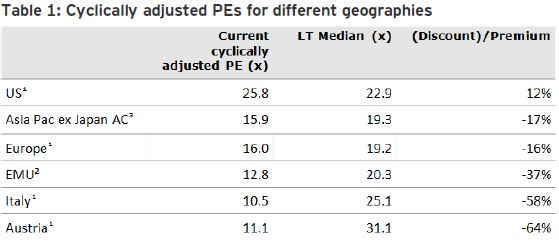

Indeed, Italy - and Austria for that matter - stand out as already having had a monster de-rating, as the following table of discounts to long term Shiller PEs shows (see Table 1).

Source: JP Morgan Cazenove, Thomson Datastream as at 30 November 2016. 1Underlying data started from 31 January 1970 for MSCI Europe, MSCI US, MSCI Italy, MSCI Austria.2Underlying data started from 31 January 1973. EMU Datastream index. 3 Index captures large and mid-cap representation across 4 of 5 Developed Markets countries excluding Japan and 8 Emerging Markets countries in the Asia Pacific region. Underlying data started from 31 December 1987. MSCI AC Asia Pacific ex-Japan index. Current cyclically adjusted PE (x) as at 30 November 2016. All cyclically adjusted P/E data based on 10 year average nominal earnings.

So what next? A bout of political shillyshallying of the kind Italy is so good at is highly likely. President Mattarella will be working on a caretaker government. It seems unlikely that Renzi will be involved given the extent of the loss.

What does seem highly unlikely is that Italy will end up having early parliamentary elections (due by spring 2018). Self-serving politicians may want to hang around to the end of the current parliamentary mandate: in Italy it guarantees you a generous pension for life! There is a clear majority in parliament for a change of the country's election laws and from what we understand this is likely to be done in a way which will go back to making it very hard for a single party to end up in power. From a market perspective, if that makes it harder for the populist radicals Movimento 5 Stelle (5 Star Movement) to get into power, then that's a good outcome.

Italy needs reform so the referendum results are a proper setback. It also needs the successful recapitalisation of the bank MPS, which is underway and has just been made more complicated. Some are suggesting that investment by the Italian state in this is now more likely. Unicredit is also limbering up to raise capital: this bank, in which some of our funds are invested, does at least have more than one lever to pull and is currently in talks to sell major assets.

This is not in our opinion a 'Brexit 2' moment. The European Central Bank said before the vote that it is ready to act in the Italian government bond market (BTP) if Italian debt comes under pressure. One similarity with the aftermath of the Brexit vote though is that many sell side commentators are already saying that the right stocks to own (in Europe then and in Italy now) are in the 'risk off category': that proved to be wrong then and, after some initial volatility, could well prove wrong now.

The Italian market and especially the cyclical elements of it are already very lowly valued in a historical context. Our funds are generally overweight Italy - actually not that difficult when the entire country weighting is only about as big as Nestlé in Europe ex UK indices! That Italy was holding a referendum and that it was likely to be a No and that Renzi would resign in the event of a No, should after all not really be new news to anyone. Fear generates opportunities.