Being prepared by planning for your retirement is crucial but it doesn’t have to be difficult.

Invesco as your pension partner can help you navigate the investment landscape.

Reflect changes in personal circumstances

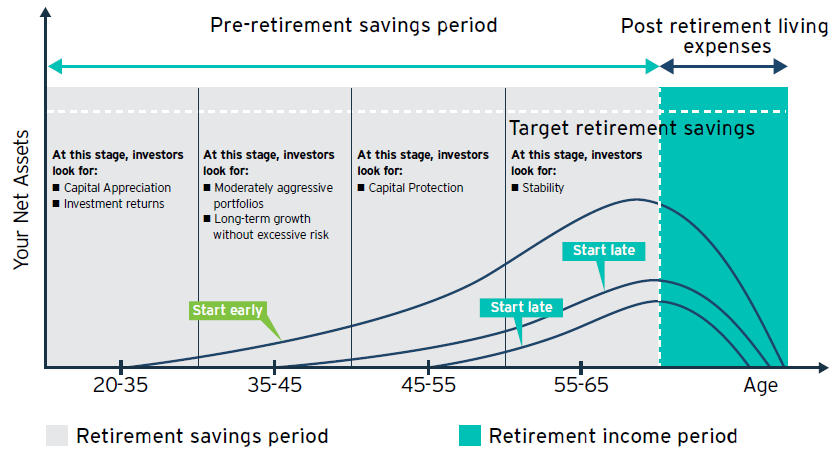

Investing in a pension scheme allows you to plan your retirement more effectively. The number of years you have until retirement helps determine the best way to grow your investments. As move into each life stage, your needs and preferences are likely to change along with your investment decisions.

What you need to know

Consolidate your accrued benefits

When you change jobs, you also need to take care of the pension investments made during your previous employment, typically referred to as "Accrued Benefits", which may be from MPF or ORSO schemes.

Accrued Benefits are defined as the amount of an employee’s beneficial interest in a retirement scheme at a particular time (such as the statement end-date). The beneficial interest is calculated as the contributions made by the employee and employer, together with any investment return (gain or loss) on the contributions.

If you have changed jobs more than once, you probably have one or more personal accounts with accrued benefits. If you remember how many personal accounts you have and which service providers are managing those accounts you can consolidate.

For Fund transfer form, Personal account membership form, Enrollment form and MPF scheme brochure/ Prospectus, please click here.

Build more wealth

Increasing your pension contributions is important to ensure you can enjoy retirement. Many people underestimate the amount they should contribute, leading to a shortfall in pension benefits.

Case study

Name: Edmund Chan

Age: 20

Retirement Age: 65

Current monthly income: HK$10,000

Expected income growth rate: 5% p.a.

Employee's contribution to retirement plan: 5%

Employer's contribution to retirement plan: 5%

Project average return of pension investments: 6% p.a.^

Edmund’s pension amount when he retires = HK$5,891,591

Amount needed by Edmund when he retires = HK$8,230,673

Retirement shortfall = -HK$2,339 ,082

Edmund could avoid the shortfall with an additional monthly contribution of only HK$1,443 per month.

Assume Edmund Chan needs to have 70% of his pre-retirement monthly income every month during retirement years to maintain his current living standard.

^ Assume the investment return to come down to 3% p.a. after retirement because Edmund Chan will likely invest in asset classes with a lower risk/return profile.

Above amounts are shown in today's value.

Make use of flexible voluntary contributions

Flexible Voluntary Contributions (FVC) available under the Invesco MPF Scheme are a great way to avoid retirement shortfalls and easy to start doing!

You can:

- Withdraw your FVCs at anytime

- Mix & match within the Invesco MPF scheme to suit your needs

- Make lump sums anytime or arrange monthly contributions (min HK$1,000) through direct debit

- Simply call or login to manage your account

For Flexible Voluntary Contribution Form, Personal account membership form, Enrollment form and MPF scheme brochure/ Prospectus, please click here